Oklahoma’s Storm Damage Problem Didn’t End When the Weather Cleared

Unresolved hail storm insurance claims remain a burden for many homeowners heading into the 2026 spring storm season. Hail, storms with high winds, tornadoes, and flooding hit communities across Oklahoma last year. Many people realized too late they had homeowners insurance coverage gaps that left them shouldering the costs of the damage. Some insurers delayed payment, underpaid, or completely denied legitimate claims.

That’s why many have turned to McIntyre Law for help in getting the compensation they deserve and paid for, taking action against insurance companies acting in bad faith.

Why Some Oklahomans Are Still Fighting Insurance Companies Over Last Year’s Storms

An unusually high number of severe storms damaged property across Oklahoma last year. Powerful straight-line winds and large hailstones pounded roofs, cracked siding, shattered windows, and inflicted structural damage that wasn’t always visible. The destruction didn’t come from just one storm. Round after round of severe weather complicated the claims process for hail storm insurance coverage.

The storms left many asking, “Does homeowners insurance cover hail damage?” You’d think so, but the claims denial rate has skyrocketed. Insurers scrutinized each claim, categorizing some damage as merely cosmetic and deeming other claims as unrelated to the storms. Even when reimbursing homeowners, payments have often been far below the actual cost of repairs.

Homeowners have tried to challenge insurance companies only to be met with demands for costly inspections and mountains of paperwork. It’s easy to get lost in the complex language of coverage documents. Without expert help, the average person may get tied up in endless red tape and struggle to ever get fully compensated.

Common insurance issues faced by homeowners in 2025

Many Oklahoma homeowners faced frustration and unexpected costs after last year’s storms. Instead of a smooth, supportive process, they encountered difficulty after difficulty:

- Insurance claim denials after a storm or several storms

- Partial payments for major repairs to roofs, siding, and structures

- Long delays and red tape with inspections, approvals, and endless processing

- Disputes over the severity of damage

- Repeated requests for more documentation

People with wind and hail insurance in Oklahoma may have thought they were protected from losses. Unfortunately, all their premium payments got them were delays, money woes, and added stress when they needed help the most.

How insurance companies respond to widespread storm damage

After waves of severe storms swept across the state, insurance companies were inundated with claims. As changing weather patterns bring more storms and severe weather, there’s more property destruction. For insurance companies, this means a higher risk of having to pay claims.

One way insurance companies deal with increasing risks is to tighten their review processes. They’ll interpret coverage more narrowly, apply stricter standards, and look for ways to avoid paying for a full repair or replacement. They may turn to low-cost vendors willing to cut corners when it comes to conducting inspections, providing repair estimates, and actually doing the work. It’s all about protecting profit margins.

While you may think you have good hail storm insurance, you might not be able to get adequate reimbursement for your losses. Your insurance company may even deny compensation altogether.

Preparing Your Home for the 2026 Storm Season in Oklahoma

Getting ready for spring storms starts with reviewing your wind and hail insurance in Oklahoma. Make sure you understand the terms of your policy, and look for potential homeowners insurance coverage gaps.

Beyond reviewing your hail storm insurance, there are a few steps you can take to lower your risk of storm damage and prevent insurance disputes, delays, and insufficient reimbursements for your losses. Act now to be in the strongest possible position before storm season.

Important home maintenance and upkeep

A well-maintained home can weather storms better than one that needs repair. Minor problems can lead to serious damage when your home is hit by wind, water, and hail. Inspect your property now, and secure or fix any issues. Performing a detailed inspection now can also support your position if you need to file a wind or hail storm insurance claim. Here’s what to do before the coming spring storms arrive:

- Inspect your roof, looking for leaks, weak spots, sags, collected debris, and cracked, curling, or loose shingles.

- Secure structures and landscaping. Fasten down gutters and shutters, repair fences, and make sure trellises and yard ornaments can withstand high winds. Reinforce sheds and outbuildings.

- Prune tree branches so that trees don’t catch as much wind. Clear brush and debris, and cut down any trees that could fall on your house.

- Clear your property of items that can become projectiles in high winds. These include things like toys, yard ornaments, and patio furniture.

Document your home before a storm hits

Record evidence of your home’s current condition. Take pictures of your property from multiple perspectives, both inside and out and from up close and afar, to document how things look before storms hit.

Keep receipts, repair records, and documents related to upgrades and maintenance to prove the condition of your home and its value. Store multiple copies of these important documents in several locations in case they’re damaged or destroyed in your home. Better yet, make digital copies and store them online. You’ll have ready access should you need to make a claim on your wind or hail storm insurance coverage.

Prepare Yourself Legally Before You Need to File a Claim

By checking your insurance policy before storm season, you can lower your risk of a claim denial, prevent disputes before they start, and ensure you get the full wind and hail storm insurance coverage you pay for and are entitled to. A wind and hail storm insurance checkup can uncover gaps, give you the chance to clarify confusing terms, and close any loopholes your insurer might use to limit or deny your claim.

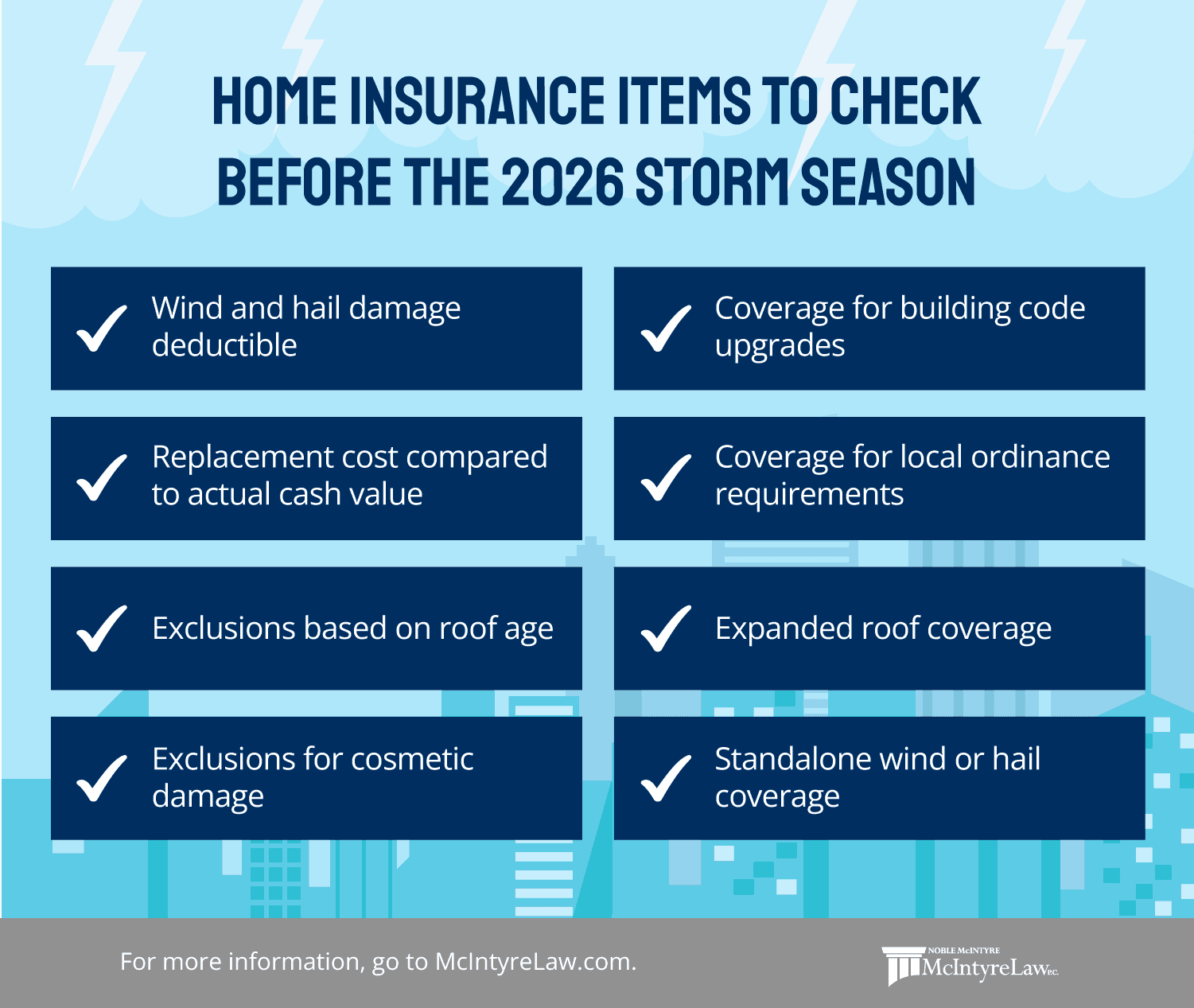

Key points to check in your homeowner’s policy before the 2026 storm season

- Wind and hail deductible: This is the set amount you have to pay out of pocket before insurance kicks in. It’s often calculated as a percentage of your home’s insured value. Knowing the exact dollar amount helps you budget to set aside money in advance.

- Replacement cost vs. actual cash value: The replacement cost covers what it takes to repair or replace something. The actual cash value only pays for what something is currently worth. The actual value of an old door or window is less than the cost of a new one.

- Roof age exclusions: Insurers know that when a roof fails, the damage can be significant and expensive. They may specify reduced payments for roofs beyond a certain age.

- Cosmetic damage exclusions: Your insurer may specify that certain damage can be classified as only affecting appearance, not function. They may use this point to deny paying for dented siding or cracked roof shingles.

Insurance coverage options worth considering

- Code upgrade coverage: Make sure your coverage includes rebuilding or replacing damaged parts of your home to meet current codes, which may be more expensive than previous standards.

- Ordinance coverage: Ordinances may be different now than when your structure was originally built. You might need to change the pitch of your roof, add safety features, or observe a setback, which can add to your costs.

- Increased roof coverage: Look at your policy details to see if it limits this kind of coverage. You may be able to pay to add coverage to completely protect vulnerable roof structures.

- Separate wind or hail coverage: Does homeowners insurance cover hail damage? It can, but you may need to add a specific hail storm insurance coverage rider to make sure your property is fully covered in an Oklahoma storm.

What to Do if a Storm Damages Your Home This Spring

Think through your action plan now, before the stress and chaos that comes with surviving a storm. Repair crews, contractors, and insurance companies may be overwhelmed in the storm’s aftermath. Having a plan can focus your efforts on a faster, smoother recovery.

Take these key steps:

- Contact your insurance company immediately to get ahead of the flood of claims. The sooner you call, the sooner things get moving.

- Take photos of the damage as soon as you can. Keep receipts for emergency repairs and damage mitigation.

- Prevent further damage. You might move belongings out of flooded areas, cover broken windows, and place a tarp over a damaged roof.

- Get estimates to document the cost of repairs, and establish relationships with contractors before they get booked up.

Warning signs of a possible insurance dispute

If you haven’t made a claim on your wind and hail storm insurance coverage before, the process can be confusing. Here are some signs that your insurance company may not be handling your claim fairly:

- Delaying, postponing, or rescheduling inspections repeatedly

- Providing conflicting explanations from different insurance adjusters

- Pressuring you to settle quickly for a low payout, or giving you little time to review the offer

- Making complicated requests for documentation and more evidence of your losses

- Offering a partial payment or a payment much lower than you expected without explanation

If you notice even one of these warning signs, take it seriously and act quickly. Keep careful records of your damage, the steps you’ve taken, all communications, and photos that document your losses. Consider working with a qualified professional who can guide you through the claims process and help you communicate effectively with your insurance company. When you have help, your insurance company is more likely to handle your claim fairly.

Looking Ahead to Spring Storm Season in Oklahoma

Every Oklahoma resident knows that storms are part of life in this area. That doesn’t mean you need to simply accept it when an insurer fails to treat you fairly. Prepare your home, your finances, and your insurance coverage to weather spring storms with confidence.

McIntyre Law stands up for Oklahomans

You don’t have to go it alone against your insurance company. Suffering a loss is stressful enough without having to fight for fair treatment. McIntyre Law helps homeowners in Oklahoma hold insurance companies accountable and get the benefits they pay for and deserve.

If you suspect your insurance company isn’t fulfilling its promises to you, call McIntyre Law. We protect your rights and fight for every penny of coverage due.